Inflation and your car insurance premium – What you need to know

When inflation is high it drives up the costs associated with vehicle repairs, which ultimately has a knock-on effect on your insurance premium.

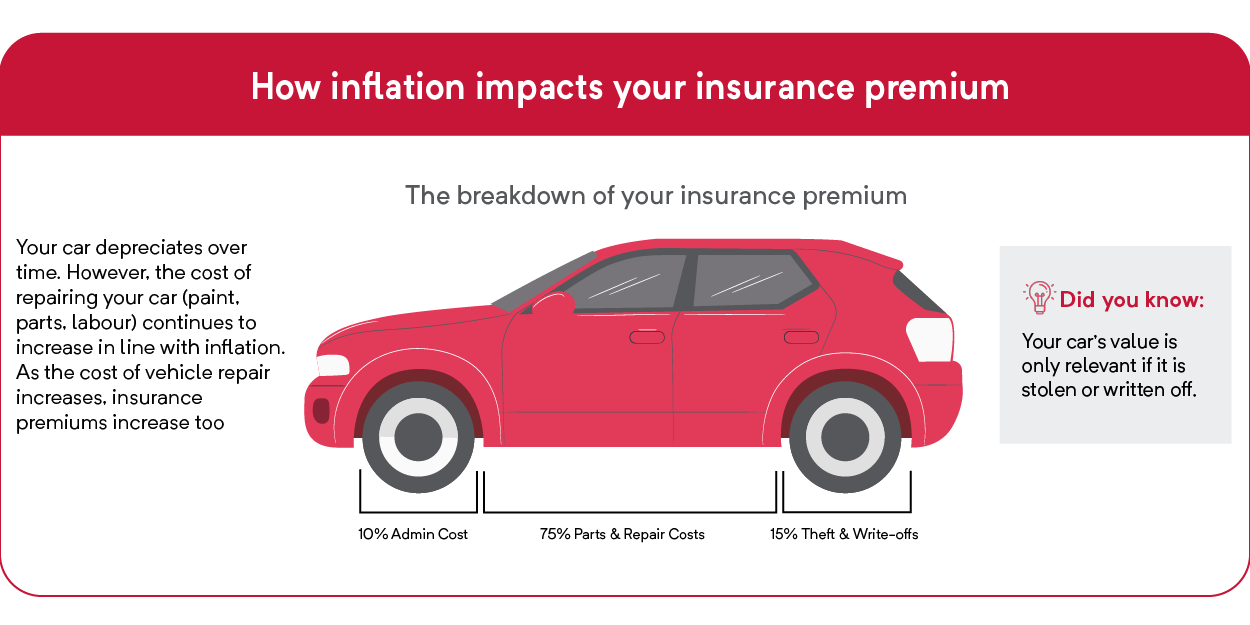

Despite a car depreciating as it gets older, it’s not insured for its replacement value, but rather for what it will cost to repair.

“Insurers report that most claims are a result of accident damage. This means the insurer carries a greater risk of paying for accident damage than they do for vehicle theft or total write off,” said MotorHappy, a supplier of motor management solutions and car insurance options.

“As a result, a greater percentage of your premium goes towards the risk of accident damage.”

Therefore, as inflation rises so, too, does the cost of labour and replacement parts, which in turn drives up motorists’ monthly insurance premiums.

“For example, if your car side mirror needs to be replaced after an accident, the cost of the mirror and the labour associated with the repair will be high, regardless of how old your car is,” said MotorHappy.

The issue could be exacerbated if you drive a rare car of which there are few others on the road, one that was discontinued after it was purchased, or one whose parent brand has since left the country.

The below infographic supplied by MotorHappy breaks down where your car insurance premium goes.

More factors affecting your premium

Past the sum of your car’s parts, your monthly insurance premium is affected by various factors, including:

- Type of car

- Purpose of the car

- Where the car “sleeps”

- Claims history

- Level of coverage

- Owner age and gender

- Excess amount payable

While elements such as your claims history and age and gender can’t be changed, other factors can be reviewed to ensure that you’re paying as little as possible per month while still getting adequate coverage.

Choosing a higher excess amount, in other words the amount you are liable to pay in case of an accident or theft, will lower your premium.

“However, if you choose a high excess amount to get lower monthly premiums, be sure that you are in a financial position to pay the excess if your car needs to be repaired or replaced,” said MotorHappy.

Additionally, if you move into a new neighbourhood or start parking your car in a more secure area it could bring down the premium further and this should be communicated to your insurer.

If you can no longer afford comprehensive coverage, the most expensive type of insurance, it might also be better to choose a cheaper level of coverage such as third-party, fire, and theft; or just third-party, rather than completely canceling insurance.

Keep in mind, though, that if a car is financed the bank will likely require it to have the comprehensive package, said MotorHappy.