South Africans are taking out bigger car loans – And paying the price for it

Motorists are increasingly relying on long-term contracts to finance their vehicle purchases in South Africa.

This is according to Lightstone Auto, which recently published its new analysis of car sales data.

A concerning trend that emerged from the data is that the vast majority of car purchases made in the last 10 years have extensive payback times.

The average car loan in South Africa now spans 72 months (six years), which is reflective of the broader cost of living crisis.

More and more people are struggling to make ends meet, which has resulted in several changes to the automotive landscape.

Many households are downsizing from two cars to just one, and the payment periods for those cars has gone up substantially over the last 10 years.

A longer finance contract means that the monthly instalments owed on a new car are smaller, which brings a measure of short-term economic relief for individuals living paycheck to paycheck.

However, it also means that consumers are paying more for their vehicles over the long term, as lengthy finance plans lead to significantly more interest that needs to be paid off on top of the vehicle’s purchase price.

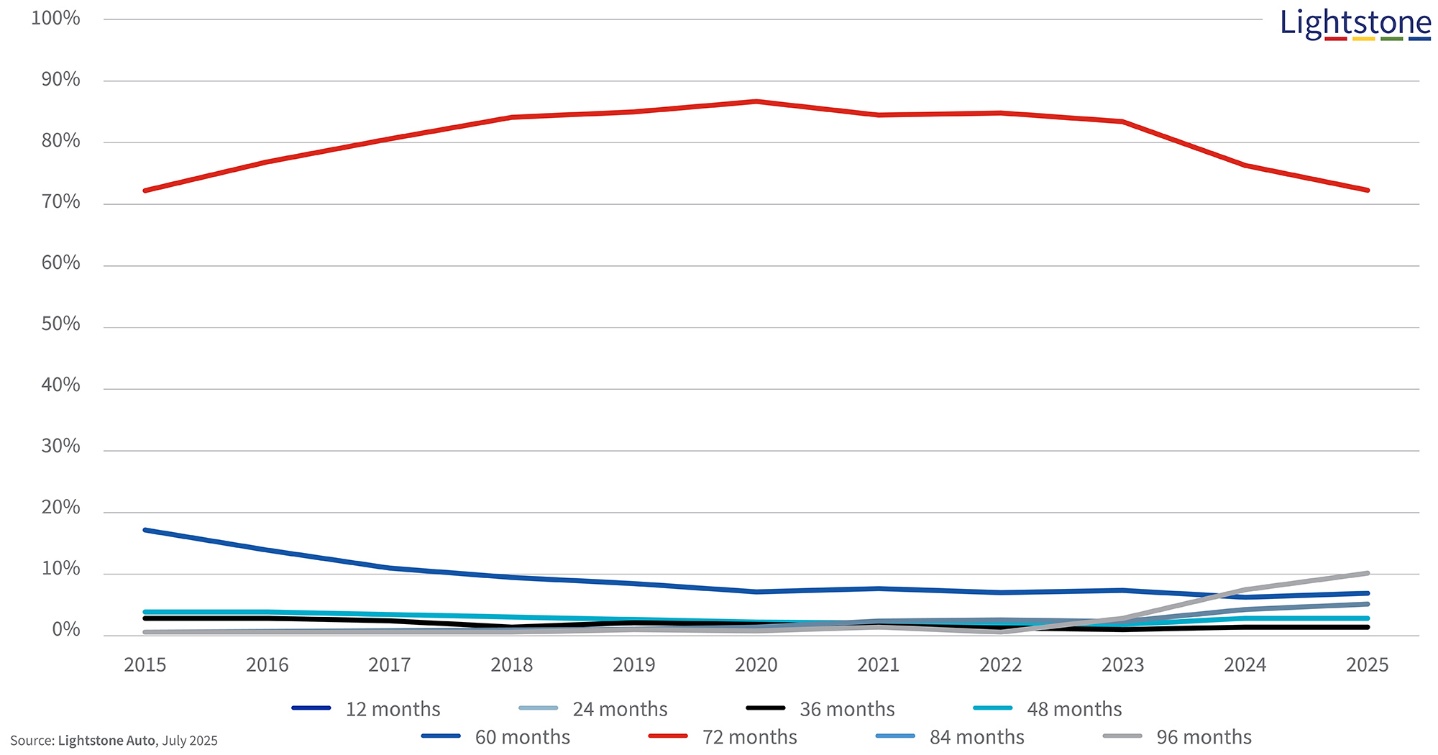

The following graph shows the frequency of different car loan periods in South Africa from 2015 to 2025, as provided by Lightstone:

Buying a car in 2025

To get a sense of what this looks like in practice, we calculated the true cost of a finance plan for a Toyota Corolla Cross – one of the best-selling vehicles in the country.

An entry-level Corolla Cross Xi retails for R414,800, and the prime interest rate is currently pegged at 10.50%.

Most South Africans also don’t put down a deposit when buying a car.

Based on these factors, a buyer with a 72-month contract would need to pay R7,881.19 per month.

This means that, by the time they finally pay off their loan, they would have spent a total of R567,445.68.

That’s a difference of R152,645.68, which is 36% more than the initial purchase price.

“In 2015, the 72-month repayment window accounted for 73% of deals, and this six-year window has remained the standard with respect to vehicle financing, growing to as high as an 87% share in 2020, before moving back down into the 70s with a 72% share currently in 2025”, said Andrew Hibbert, Lightstone Auto Data Analyst.

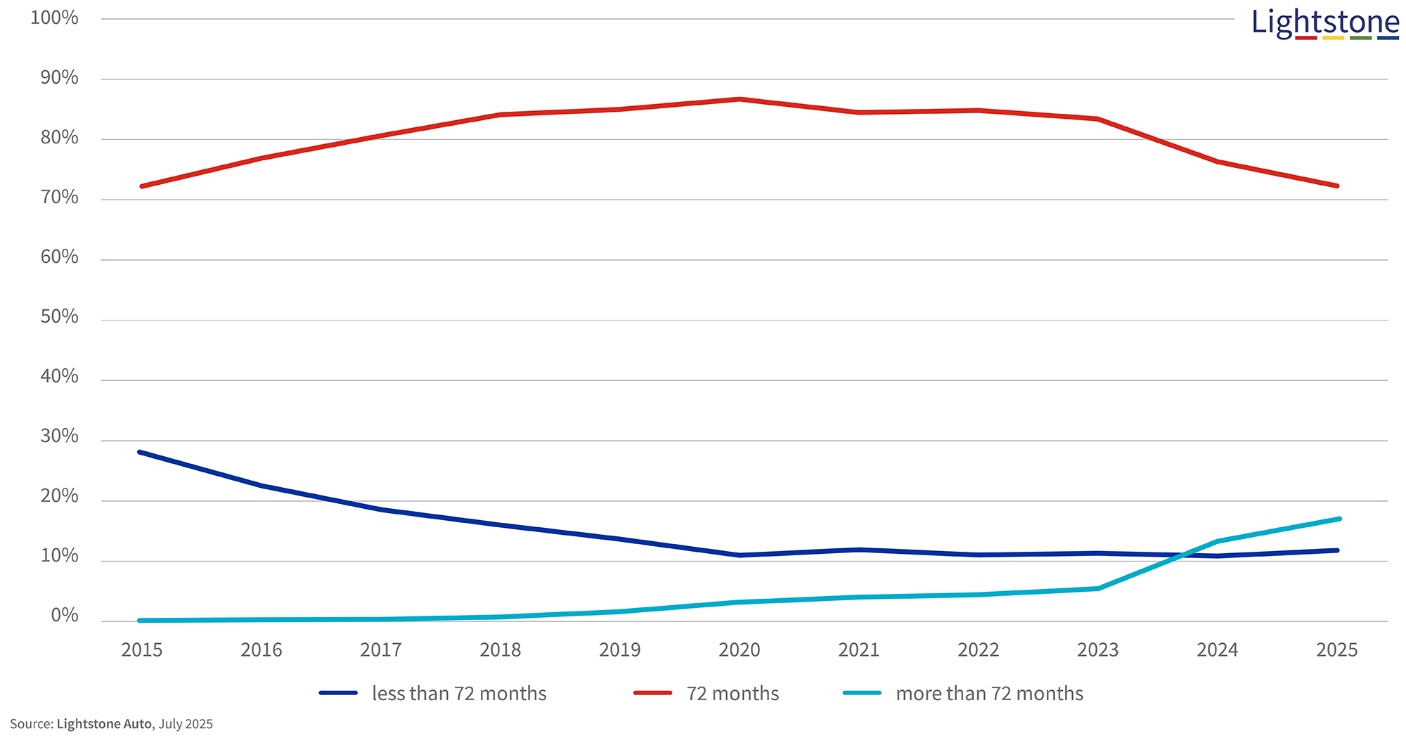

While it may seem like good news that 72-month contracts are declining, this is only because even longer payment plans are starting to take off.

This is illustrated in the graph below:

In 2015, a 60-month (five-year) loan was the second most popular option for car buyers.

Contrast this with 2025, where a 96-month (eight-year) term is now the second most popular finance solution.

It’s another sign that cars are becoming unaffordable to many consumers, who are resorting to more extreme policies to obtain a set of wheels, even if it means they are paying far more in the long term.