Volkswagen CEO Oliver Blume is coming under mounting pressure from shareholders to show his overhaul is moving fast enough, as BMW’s deep outlook cut adds to concerns over prospects for Germany’s auto industry.

At VW’s annual meeting on Thursday, investors will ask if efforts over the past three years of Blume’s tenure are enough as China’s electric-vehicle champions reorder the industry.

At stake is Europe’s biggest carmaker’s ability to finance its future and keep paying the dividends that help sustain its investor appeal.

Blume can point to some progress: development costs are falling, VW is leading EV sales in Europe, and new models are reaching customers faster with fewer quality problems.

But VW is still grappling with US tariffs, a persistent weakness in China and its own complexity, prompting Blume to pursue additional reductions.

“Without a decisive restructuring, Volkswagen risks a gradual decline,” said Tanja Bauer, a sustainability and corporate-governance specialist at Deka Investment, one of Germany’s largest fund companies. Shareholders need “a business model that reliably produces returns again.”

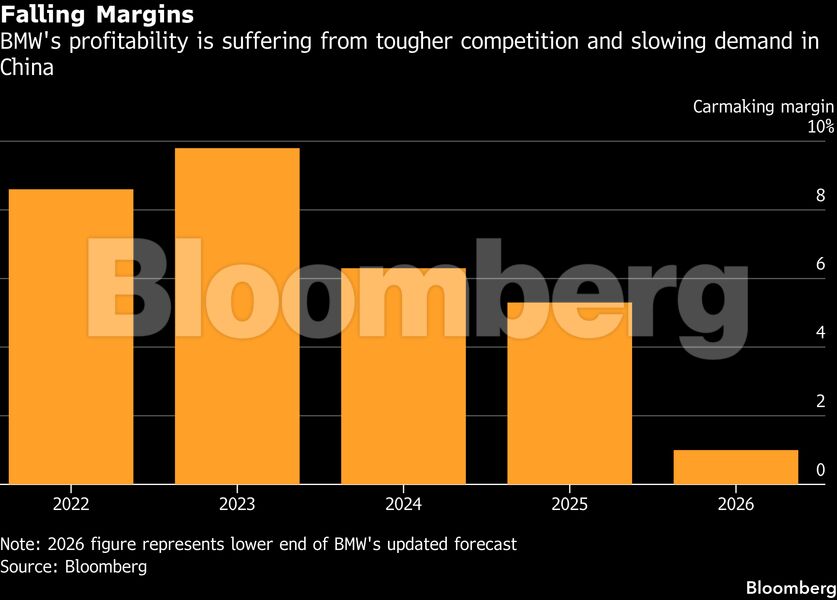

VW’s outlook — it currently sees an operating margin of at least 4% this year — is under pressure after BMW this week slashed expected carmaking returns to as low as 1%.

The luxury rival to VW’s Porsche and Audi brands said the move to cut guidance from as high as 6% was prompted by the slump in China and weaker buying appetite elsewhere due to the conflict in the Middle East.

China is the most acute concern. Car sales there declined by more than a fifth in May, with demand for combustion-engine vehicles — still the mainstay for both VW and BMW — dropping nearly 40%.

The deterioration prompted forecasters, including the China Passenger Car Association, to sharply downgrade their annual sales outlook.

While German carmakers are churning out fresh products, partly through new partnerships, steep discounting and more nimble local competitors risk leaving them priced out of the world’s biggest passenger car market.

BMW is succumbing to the same pressures that have hit VW and Mercedes-Benz, raising questions about the German luxury car business model and the longer-term viability of exporting vehicles from Europe’s biggest economy.

Both VW and Mercedes have been shedding jobs and cutting production capacity.

The “radical earnings cut” is a “wake-up call for the auto industry,” JPMorgan analyst Jose Asumendi said in a note.

At VW, Blume has made some big changes. The latest move is a plan to sell a marine engine unit that could be valued at €8 billion (R150 billion) or more.

Some 28,000 workers have already agreed to leave VW, and the company has whittled down its production capacity from 12 million vehicles a year toward a more realistic 9 million.

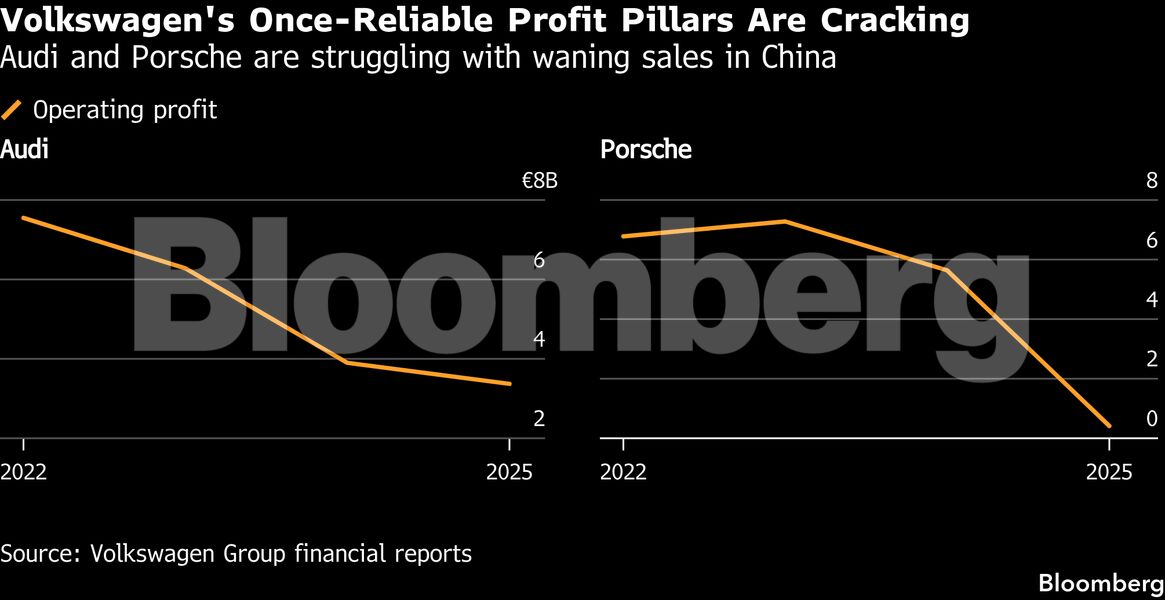

The problem is that the world has moved on, too. VW’s former cash cows, Audi and Porsche, are especially exposed to President Donald Trump’s tariffs as the brands import all of the cars they sell in the country.

The pressure is not confined to China. The same local champions that have eroded German automakers’ position there have muscled into Europe and are setting up local production, intensifying competition in a market that for years has seen only muted growth.

Volkswagen’s peers, Stellantis and Renault, face similar challenges, resulting in investors increasingly questioning whether owning shares in European carmakers is worth the risk.

VW’s profitability gap is part of that anxiety. Blume targets an operating return of 8% to 10% by 2030 to fund dividends as well as spending on EVs and software.

To get there, he must streamline a group spanning mass-market cars, luxury brands, finance, software, trucks and legacy industrial holdings — scale that once made VW formidable but now risks becoming a drag.

The clearest expression of that complexity is VW’s product range. The group sells more than 150 models, from budget Skodas to Porsche 911 sports cars, across regions with sharply different demand profiles.

The VW Golf, Seat Leon and Skoda Octavia all compete in the compact-car space, while SUVs such as the VW Tiguan, Skoda Kodiaq, and Audi Q3 chase overlapping buyers at different price points.

That breadth once helped the company squeeze scale from every corner of the market. Now it leaves VW with high costs and a slower response compared to rivals that develop cars more quickly.

Stellantis is dealing with a similar overlap and has started inviting in Chinese rivals to deal with excess capacity.

There still is a bull case, however. Audi is accelerating its overhaul with new models, including a large SUV tailored to US buyers and deliberations to sidestep tariffs there with local production.

Porsche’s new CEO, Michael Leiters, has pledged more cost cuts and is planning an investor day in the fall to explain how the brand can rebuild margins.

In China, VW is trying to recover lost momentum with a strategy built around faster development, more affordable engineering and partnerships with local manufacturers such as Xpeng and SAIC.

If that works, China could become a source of speed for the group.

But Volkswagen shareholders have seen false dawns before. Since the diesel crisis, the group has repeatedly promised to become nimbler, only to run into the weight of its own structure.

For Blume and his predecessors, the problem has never been the absence of a plan.

The harder task is punching through pushback from within the group, with strategy pivots requiring approval from labour leaders, state politicians and the powerful Porsche-Piëch billionaire owner family that depends on steady dividends.

VW’s ownership structure “makes substantial change very difficult,” said Christian Strenger, a shareholder and corporate governance expert.

“Oliver Blume is trying his best, but with this supervisory board, serious cuts are extremely hard to imagine.”